WASHINGTON — Out of 30 of the largest companies in the United States last year, nearly a quarter paid more to their chief executive than they did in federal taxes, according to new research.

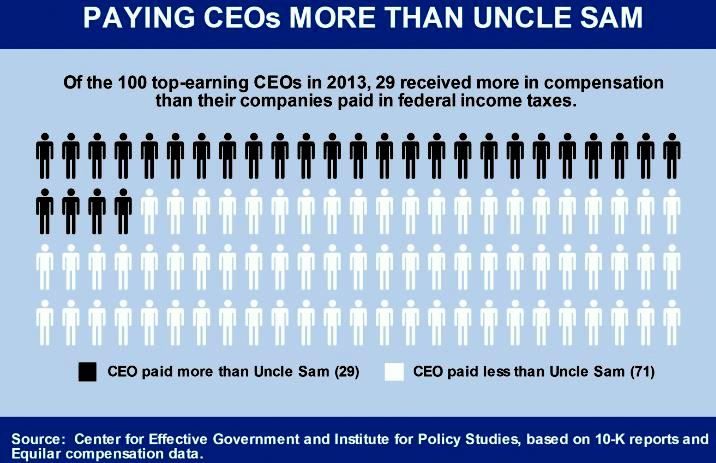

That proportion appears to hold true for a larger sample of U.S. companies, as well. Of the country’s 100 top-paid CEOs last year, 29 received more in compensation than their companies paid in taxes. And that trend appears to be strengthening.

“The last two times we looked at these figures, 25 out of the top 100 fell into this category. This time it’s gone up to 29,” Sarah Anderson, director of the Global Economy Project at the Institute for Policy Studies, a Washington think tank, and co-author of the new report, titled “Fleecing Uncle Sam: A growing number of corporations spend more on executive compensation than federal income taxes,” told MintPress News.

“So clearly there isn’t a lot being done to crack down on the massive tax loopholes that these very large corporations, in particular, are able to take advantage of. In fact, the problem is getting worse.”

This was the first time that the report, jointly produced by the Institute for Policy Studies and the Center for Responsive Government and released last week, has included exploration of the compensation and tax-payment practices of the country’s 30 largest companies. Project organizers call the findings “shocking.”

Of these, the seven companies that paid their CEOs more than what they paid the U.S. Treasury are among the most well-known names and brands in the world – Boeing Co., Ford Motor Co., Chevron Corp., Citigroup Inc., Verizon Communications Inc., JPMorgan Chase & Co. and General Motors Co. Further, each of these corporations was extremely profitable in 2013, collectively taking in some $74 billion in profits before taxes, according to estimates in the new report.

Yet these companies were also able to make use of a spectrum of tax breaks that resulted in significant refunds. Using public information, the researchers were able to estimate that these seven companies got back nearly $2 billion in tax refunds for last year. That would result in “an effective tax rate of negative 2.5 percent,” the report states.

Most of these companies were unavailable for comment by deadline, though several have disputed the report’s methodology. A Verizon spokesperson told MintPress that the report is “inaccurate,” noting the company “paid 2013 federal income taxes that were exponentially greater than its CEO’s compensation.”

Yet the report suggests that similar figures result from running the numbers for the companies run by the top 100 highest-paid CEOs. The 29 of these entities that paid their top executive more than they paid in taxes made some $24 billion in profits before taxes, and claimed $238 million in refunds. The result, again, was an effective tax rate of negative 1 percent.

“If these companies are so profitable, what’s the argument for why they shouldn’t be contributing to the Treasury?” Anderson asked.

“While this is a reflection of these companies’ ability to hire hundreds of lawyers to find and exploit these tax loopholes, ultimately this is very shortsighted policy. These companies need public investment in the infrastructure, health care and all the other inputs that make this a highly functioning economy.”

In the long run, Anderson says, erosions in public investment will ultimately hurt major corporations – just as they hurt everyone else.

The extenders debate

The researchers are not accusing any of these companies of breaking the law. Rather, the corporations are making use of a spectrum of tax exemptions, subsidies and loopholes that have accumulated over the course of decades of tax-writing and corporate lobbying.

Indeed, the new data comes out just as federal lawmakers are debating what to do with around 55 tax breaks that would need to be extended by the end of this year. These are not new policies, but an already expired group of favorable tax policies put in place “temporarily” then regularly extended by Congress, typically with relatively little debate. For this reason, these policies are often referred to as “extenders.”

Some of these provisions cover generally well-regarded subsidies for, for instance, research and development. Others offer industry-specific giveaways that have long been the brunt of both criticism and public mockery – exemptions for NASCAR tracks, for example – but which get extended anyway.

In part because of the fiscal debate that has seized Washington in recent years, last year Congress did not move forward on renewing the extenders, resulting in the significant pressure on lawmakers today. Nearly all of these are expected to be extended once again, though.

According to the new report, some 80 percent of these extenders are for business.

“The House has already passed a permanent extension of five tax breaks for businesses, which will cost more than $500 billion over the next decade. The two-year Senate package will cost $85 billion, more than 80 percent of which will go to corporate tax breaks,” the report states.

“While deficit hawks often call for programs benefiting ordinary American families to be fully paid for with cuts to other social programs or new revenue offsets, they do not place the same demands on corporate tax cuts.”

This concern heated up significantly on Monday, following media rumors that the House and Senate were close to an agreement on the extenders package. Early reports from The New York Times suggested that the deal would make several corporate tax breaks permanent, without offsetting this funding deficit elsewhere. In addition, it would apparently drop certain key tax provisions widely seen as helpful for low-income families.

While there is no firm evidence of the contours of any such deal, these reports clearly worried President Obama’s administration. On Monday, Treasury Secretary Jack Lew came out forcefully on the issue.

“There are reports today that Congress may be considering a potential deal on extenders that would do very little for working families and would be fiscally irresponsible,” Lew said in an immediate statement.

“An extender package that makes permanent expiring business provisions without addressing tax credits for working families is the wrong approach, at the expense of middle class families. Any deal on tax extenders must ensure that the economic benefits are broadly shared.”

Later that day, the White House also weighed in on the issue, with press secretary Josh Earnest characterizing reports on the extenders deal as “not promising.”

“[T]here may be some in Congress who want to provide tax relief to businesses and to corporate insiders,” Earnest told reporters during a daily press conference, “but not ensuring that those benefits are shared by middle-class families.”

Pay for performance?

Four years after the passage of landmark legislation aimed at strengthening regulation of major U.S. companies following the financial collapse of 2008, one of the most criticized disparities characterizing today’s corporate culture – the outsized compensation offered to top executives – continues to grow.

In 1993, executive salaries were around 195 times those of average workers, according to the AFL-CIO, one of the country’s largest trade union federations. Two decades later, executives’ salaries were over 330 times larger.

“It was misaligned pay that caused bankers to blow up Wall Street in the first place,” Bartlett Collins Naylor, a financial policy advocate with Public Citizen, the public interest group, told MintPress. “But because they’re overpaid, CEOs can afford to attack anybody that makes even a small effort to reform how much money is wasted on them.”

Beyond public opprobrium, there is also mounting evidence to suggest that these extraordinarily lucrative salaries and benefits have little connection to overall corporate performance. Last week, new research found that links between executive pay and company performance are extremely tenuous.

Looking at 1,500 companies listed on the Standard & Poor’s listing, researchers with the Investor Responsibility Research Center Institute sought to explore the relationship between executive compensation, their company’s economic performance and their shareholder return.

“For the vast majority of S&P 1500 companies, there is a major disconnect between corporate operating performance, shareholder value and incentive plans for executives,” the researchers noted in a release.

“Economic performance explains only 12% of variance in CEO pay. More than 60% is explained by company size, industry, and existing company pay policy. None of those are performance driven.”