Since 2008, the Federal Reserve has more or less printed over $3.2 trillion in three rounds of quantitative easing. That’s now tapering off to zero, but many have speculated that all this printing must result in inflation simply because it puts more U.S. dollars out there than ever before.

A larger supply means the dollar should be worth less, right? In fact, it hasn’t worked out that way. Inflation remains less than 2 percent per year as it has since the financial crisis started in 2007.

It is this low because the number of dollars in the world is only one part of the equation. The “velocity of money,” or the number of times money turns over in the economy, is equally important. Data since 2007 show what every freelancer and job seeker knows — it’s a tough world out there and people are pretty slow to let go of the cash they have.

The broadest definition of “money” for which we have good data is called MZM, or money at zero maturity. This is a measure of the dollars printed and in coin, plus all bank accounts and money market accounts. It’s not a complete measure, since it does not include stocks and other investments that people can both borrow against or otherwise use to make themselves feel rich. It’s demand money — the stuff that is accessible right now.

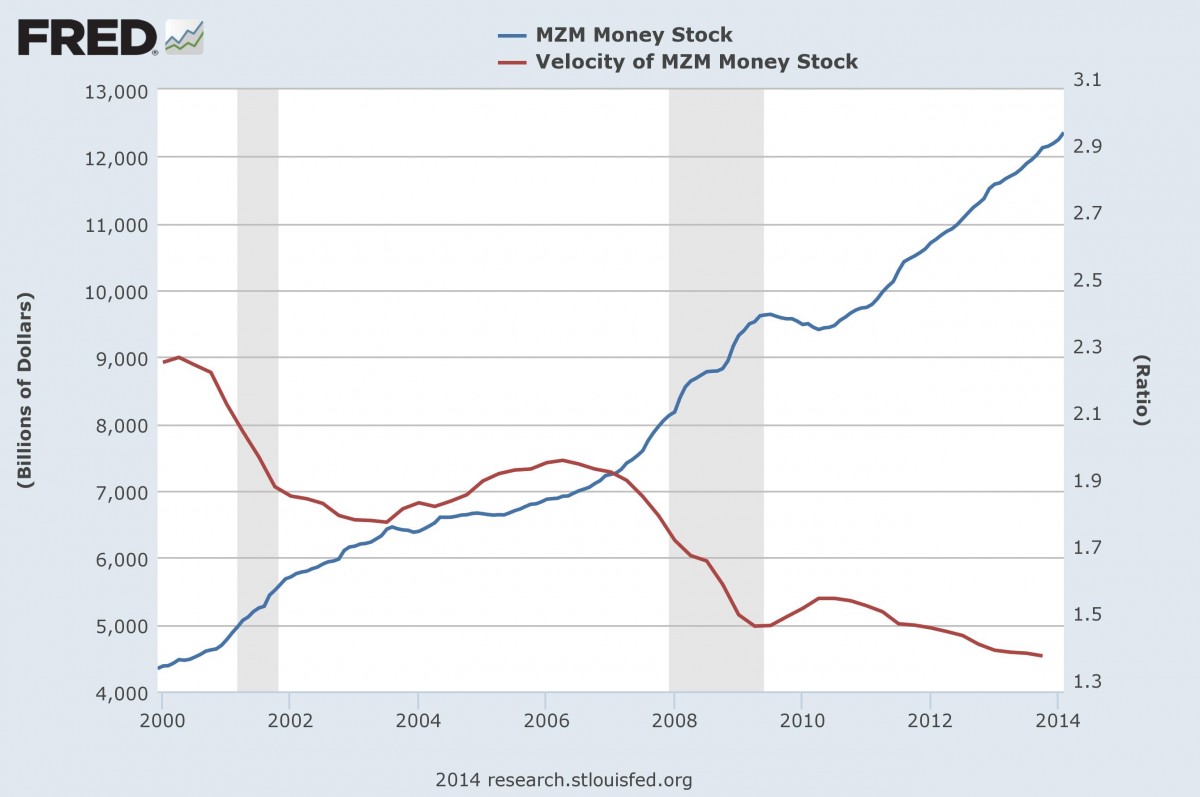

How much of that is there? About $12.3 trillion in total, and it grows all the time, as shown by the blue line on the graph below. But it has been turning over less frequently, as demonstrated by the red line:

The velocity can be taken as roughly the number of times a dollar turns over in one year through the economy. The chart above shows that coming into the current depression in 2001, it was over twice a year, but fell to 1.75 times by 2002. It never recovered to more than 1.92 times in April 2006 before it fell off a cliff in 2007 — before the “official” recession even began — where it hovers today at about 1.4 times.

What this means is that for all the money out there in the world, it feels as though there is considerably less than there has been in the past. The velocity today is only 75 percent of what it was in 2006, the last time anyone felt remotely flush with cash. Money is simply not turning over in the economy at the rate it used to.

The external effect

There is also an external effect that reflects the austerity forced on the federal budget.

The federal deficit has declined to $415 billion, or 3 percent of GDP, from a high of over10 percent as recently as 2009. This has been fueled by a large increase in tax revenues combined with a drop in spending on unemployment insurance and mortgage assistance, among other things. Our trade deficit with other nations isalso dropping rapidly due to lower fuel imports, and currently stands at less than $400 billion.

As the world continues to movetoward one big market, world trade is expected to grow at a rate of 5.8 percent this year, well ahead of the growth in world GDP.

As the$18.4 trillion in world trade, or about 30 percent of world GDP, continues to expand, the planet can expect an additional $1.07 trillion exchanged this year. By the latest estimates, 85 percent of it is still denoted in the global reserve currency, the U.S. dollar.

When China buys integrated circuits from Malaysia, it’s likely to be denoted in dollars. The same is true when Brazil sells oranges to South Africa or a European country buys oil from Dubai. There is still no currency that touches the world the way the dollar does. Many are excited that China may realize its dreams ofbecoming a reserve currency, but even thehead of the country’s central bank, Zhou Xiaochuan, acknowledged last month that Beijing still has “lots of homework” to do before that happens. The world isstuck with the dollar, at least for now.

Given the increase in world trade, we can expect a $906 billion increase in demand for dollars this year. But our trade deficit will send less than half that much overseas in 2014, meaning that demand isoutstripping supply. Hence, the value of the dollar is increasing.

Our debt, deficit and jobs

Demand for our debt is largely fueled by the same process. Treasury bills — the debt we issue to pay for our deficits — are so highly convertible worldwide that they are essentially the same as dollars, except that they bear some small amount of interest. Globally, central bankshold $3.72 trillion in Treasury bills, or about 90 days of trade. This operates as a cushion between changing currency prices as demand for dollars changes in the market. If that were to increase at the same 5.8 percent, the demand for our debt should rise by $216 billion, or 52 percent of the debt we issue. But their holdings have typically run more on the order of60 percent of the debt we issue.

There can be little doubt that the austerity that we have promoted by the process of reducing our deficit so quickly has gotten ahead of the market. The dollar has to keep rising, which means that goods made in the United States will continue to be comparatively more expensive.

Fed Chair Janet Yellen has never spoken about the foreign exchange implications of Federal Reserve policy, but she has been very explicit that the Fed’sfocus is on employment in the U.S. If we are to grow manufacturing jobs, the dollar has to stay as low as it possibly can. This suggests that low interest rates should continue, since an increase in rates makes the dollar still more valuable. If Yellen is watching manufacturing jobs, in particular, she must note that there are still6 million fewer of them than there were in 2008.

Altogether, the domestic economy is not turning over money fast enough to generate inflation domestically and our smaller trade deficit is fueling a rise in the U.S. dollar that is making imports cheaper. Both point to lower inflation for the foreseeable future and historically low interest rates for a while.