Millions of low-wage workers are being hit with fees just to access their paychecks. It’s an increasingly common trend at companies that are turning to prepaid cards instead of paper paychecks or direct deposit to distribute wages. Walgreens, Taco Bell and Wal-Mart have already adopted the prepaid cards for most employees, and many other corporations large and small are expected to follow suit. By 2014, The FDIC estimates that $60 billion in wages will be distributed to millions of workers annually using this method.

Here’s how it works: Companies can save thousands of dollars by switching to a paperless prepaid card option while banks collect fees from card users. It’s a win-win on the corporate side, but in some cases workers are held captive — unable to obtain their pay through checks or direct deposit, even when they put in a request to their employers.

The New York Times reports that Natalie Gunshannon, a 27-year-old McDonald’s worker, asked the owners of the franchise that she worked for in Dallas, Pa., to deposit her pay directly into her checking account at a local credit union. Like most credit unions, Gunshannon’s bank didn’t charge a fee for its services.

Her request was reportedly denied and she was forced to use a JPMorgan Chase payroll card that charges fees. Employees like Gunshannon believe it could constitute a form of wage theft. “I know I deserve to get fairly paid for my work,” she said.

For many, an occasional $2 withdrawal fee might seem like a minor inconvenience — part of the cost of doing business in an increasingly paperless world. The problem becomes much more acute for low-wage workers who are seeing already sparse paychecks whittled down, sometimes resulting in take-home wages less than the federal minimum wage of $7.25 per hour.

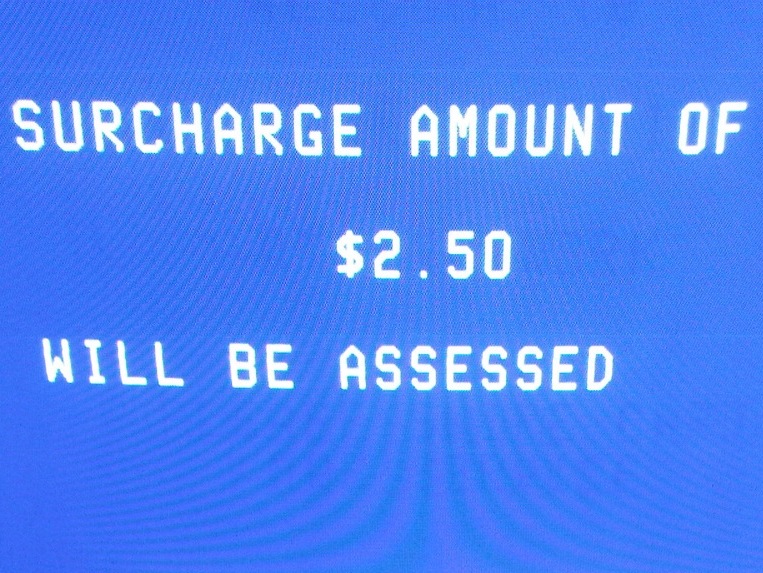

Most payroll cards charge $2 or less for making a withdrawal from an ATM and $2.95 for a paper statement. Additionally, there is usually a $6 fee to replace a lost card and some workers have reported having to pay a $7 inactivity fee for not using their cards.

Why are low-wage workers getting the squeeze? The Examiner reports that prepaid bank cards can mean big savings for large companies with hundreds of employees. Wal-Mart, a retailer with 1.3 million employees, plans to increase the use of prepaid cards for thousands of workers who do not have a bank account or opt out of the direct deposit option.

The Examiner reports that Bank of America, Wells Fargo and Citigroup are able to entice companies to adopt the prepaid cards by demonstrating how they can quickly save money. A calculator on the Visa website shows that a company with 500 employees paid weekly could save $16,900 annually compared to the cost of using paper checks or direct deposit services.

The savings to employers can be huge, but what does this mean for the average employee?

Devonte Yates, 21, who earns $7.25 an hour working for a McDonald’s restaurant in Milwaukee, says he spends $40 to $50 a month on fees associated with his JPMorgan Chase payroll card.

“It’s pretty bad. There’s a fee for literally everything you do,” Yantes said.

Previously, Bank of America proposed a $5 monthly fee for its debit card. In 2011, account holders took notice and protested the proposal. Molly Katchpole, a 22-year-old Washington, D.C., resident, launched an online petition demanding that Bank of America repeal the fee.

A month after starting the petition, Katchpole’s petition had 300,000 signatures, forcing Bank of America to reverse its decision in November 2011. Many customers left altogether, opting to bank with credit unions or local banks that do not charge fees for account holders.

Think Progress reports that many of these bank fees, including debit card fees, have been limited or prohibited through the Dodd-Frank reform bill.

Payroll cards mostly remain exempt from these type of regulations, allowing banks to recoup billions lost due to new regulations prohibiting fees on other cards and transactions.